Episode 1: Optimize the benchmark interest rate

If you plan to buy a house, you want to know how much you can borrow. How does a mortgage advisor ensure you can borrow just a little more? In the Netherlands, the maximum mortgage amount is a standardized calculation. Knowing your income, debts, (tax) mortgage history, and mortgage interest rate, you can precisely determine the maximum mortgage amount.

At Viisi, we help homebuyers optimize their mortgage potential by exploring ways to increase income and borrow more.

On this page

- Mandatory benchmark interest rate

- Percentage of your income

- Quick calculation example

- Going a step further, comparing lenders

- A practical example

- Are there any downsides?

- Are there other tricks to borrowing more?

- For the true enthusiasts: financing capacity tables

- Optimizing your mortgage based on these tables

Do you qualify for a mortgage in The Netherlands?

If you are an expat living in the Netherlands and you are considering buying a house, you may be wondering what the possibilities are for a mortgage. Use our ‘Do I qualify for a mortgage?’ tool and find out if you are qualified! No personal information will be asked when completing the tool.

Find out if you are qualifiedMandatory benchmark interest rate

One of the important variables in this calculation is the mortgage interest rate. The main rule is that the lower the interest rate, the more you can borrow. After all, the lower the interest rate, the less you spend on your mortgage. However, if the interest rate is fixed for less than 10 years, you must use a fictional rate set by the Dutch Authority for the Financial Markets (AFM) every quarter. This rate has been set at 5,0% since the year 2015.

Percentage of your income

The second factor is the percentage of your income you are allowed to use for mortgage payments. Strict rules apply here. The rules state that if the interest rate is just above a round percentage, you can assign a greater portion of your income to mortgage payments.

For example, at an interest rate of 3.51%, you can spend 25% of your income on the mortgage. At an interest rate of 3.50%, you are allowed to spend 24%. This can make a significant difference: one percent of your income to be spent monthly matters!

On a more detailed level and contrary to the main rule, you can borrow more with a slightly higher interest rate than what you can borrow for mortgage interest rates rounded to half a percent.

Quick calculation example

With an income of €60,000, at an interest rate of 3.50%, the maximum mortgage is €267,532 (2025, energy label E). With an interest rate of 3.51%, the maximum mortgage increases to €278,342—a difference of nearly €11,000!

If you want to do the calculations and better understand these variables, you can find more information on this page.

Going a step further, comparing lenders

Most people want the lowest possible interest rate when applying for a mortgage. But sometimes, it is important to be able to borrow as much as possible. What should you do then?

Do you choose a lender offering 3.51%, allowing you to borrow more, or do you prefer a lower rate of 3.4% with a smaller mortgage amount? The trick of the mortgage advisor is: you can do both!

How? You can have the mortgage amount approved on a mortgage rate of 3.51% but apply for a real interest rate of 3.4%. Is that allowed? Yes, absolutely! The maximum mortgage depends on the benchmark interest rate—and you can influence this. Here’s how:

You split the loan into two parts:

- A larger part with an interest rate fixed for 10 years or more, for which the benchmark interest rate equals the actual interest rate.

- A smaller part has an interest rate fixed for less than 10 years, for which the mandatory benchmark interest rate of 5% applies.

For the entire mortgage, the benchmark interest rate is the weighted average of both parts.

A practical example

Suppose you can apply for a €500,000 mortgage at a favorable 10-year fixed rate of 3.40%. If you apply for a small portion of the mortgage with a 9-year fixed rate, the benchmark interest rate is calculated as a weighted average:

Smart mortgage setup:

- €468,516 at 10 years fixed (3.40%)

- €31,484 at 9 years fixed (5.00%)

The weighted average interest rate is:

€468,516 x 3.40% + €31,484 x 5.00%

————————————————————— = 3.501%

€500,000

This is precisely what we were aiming for. Although you pay 3.40% interest on almost the entire mortgage, you qualify for the maximum borrowing amount based on the benchmark interest rate of 3.501%.

Are there any downsides?

Yes, here they are—along with possible solutions:

- The mortgage structure is slightly more complex

- Multiple loan parts can complicate early repayment, as some lenders impose limits (e.g., 10% per loan part).

- The 9-year fixed portion will need to be refinanced in year 10

- The interest rate at that time could be higher or lower than the current 10-year rate, which could increase monthly payments.

Want to maximize your borrowing amount? Make sure to optimize the benchmark interest rate for your mortgage!

Are there other tricks to borrowing more?

Yes! The following key factor is how income is assessed in a mortgage application. If part of your income is variable, different lenders handle it differently. Learn more in this article.

Do you want to know your exact maximum mortgage amount? Schedule an appointment with one of our experts.

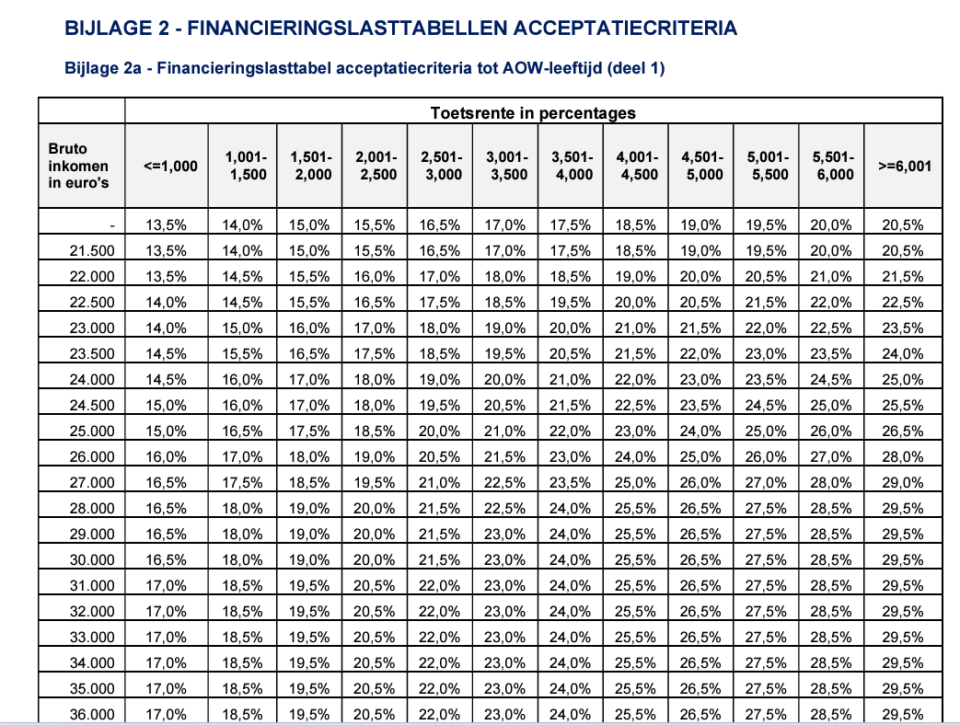

For the true enthusiasts: financing capacity tables

The exact calculations are based on so-called financing capacity tables, which are published annually by Nibud and followed by all lenders. These tables determine what percentage of your income you can allocate to your mortgage based on a specific income-interest rate combination.

Example:

- With an income of €35,000 and an interest rate of 3.2%, the financing capacity percentage is 23.0%.

- At an interest rate of 3.6%, it increases to 24.0%.

Get a free consultation to discover your possibilities

The appointment will take half an hour and you may ask any question you want.- One advisor for the whole process

- Academically educated advisors

- Advised over 15,000 home buyers

Optimizing your mortgage based on these tables

The ideal interest rate to maximize borrowing would be 1.001% or 3.501%—just enough to move the table one step to the right.

For example, if a lender offers a 10-year interest rate of 3.501%, you hit the optimal borrowing point. If market rates vary between 3.3% and 3.8%, a competent advisor calculates:

- What you can borrow at 3.3% (low rate = more borrowing according to the main rule).

- What you can borrow at 3.51% (benefiting from one step to the right in the table).

A 3.3% rate might only be available at one lender. However, the maximum mortgage at 3.51% is available at any lender offering 3.51% or lower, giving you more choices.

Depending on the additional conditions of these interest rates, you can select the best mortgage provider.